Advertisement

Taking a home loan is a 20-year commitment. Over two decades, the economy will go through multiple cycles of inflation, recession, and recovery.

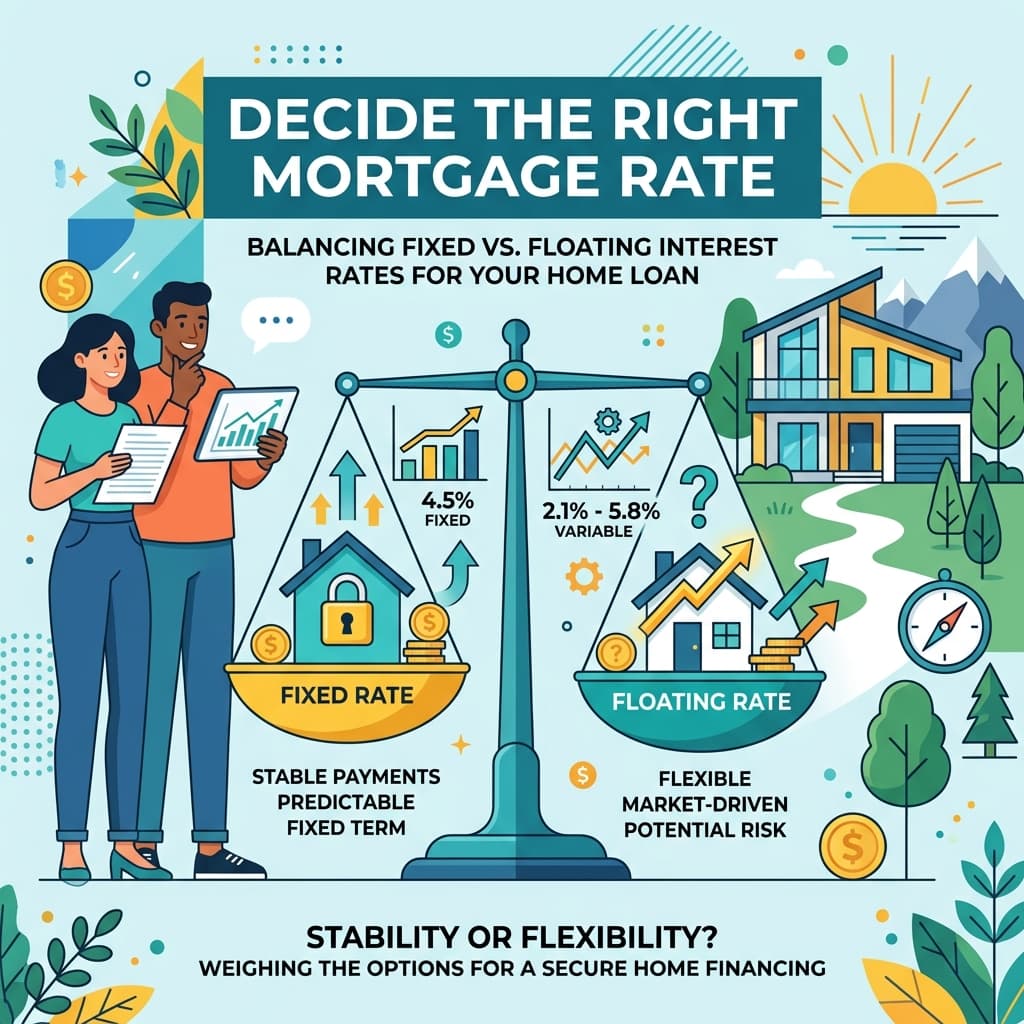

When you sit across from a loan officer, they will present you with a critical choice that will dictate your finances for the next 20 years: Do you want a Fixed Interest Rate or a Floating Interest Rate?

Making the wrong choice here can literally cost you the price of a luxury car in extra interest payments. Let’s break down the math and the mechanics of both.

Key Takeaways

- Floating is (Usually) Cheaper: Historically in India, borrowers on floating rates have paid less total interest over a 20-year period compared to those on fixed rates.

- The Repo Rate Connection: Floating rates are directly linked to the RBI's Repo Rate. When inflation is high, your EMI or tenure will increase.

- Zero Foreclosure Charges: By law, banks cannot charge a prepayment or foreclosure penalty on floating rate home loans for individual borrowers. Fixed-rate loans often carry hefty penalties.

1. What is a Fixed Rate Home Loan?

A fixed-rate home loan means your interest rate is locked in at the time of signing and will never change for the entire tenure of the loan, regardless of what happens in the broader economy.

If you sign at 9.5% today, you will pay 9.5% in year 1, year 10, and year 20.

The Pros:

- Absolute certainty. Your EMI is fixed, making long-term monthly budgeting incredibly easy.

- Protection against inflation and rising interest rates.

The Cons:

- Banks price in the risk of future inflation. Therefore, fixed rates are typically 1% to 2% higher than floating rates on day one.

- If the RBI cuts interest rates and home loans drop to 7%, you are still stuck paying 9.5%.

- Banks are allowed to charge prepayment/foreclosure penalties on fixed-rate loans (usually 2% to 4% of the outstanding principal).

2. What is a Floating Rate Home Loan?

A floating rate home loan fluctuates based on a benchmark interest rate (currently the External Benchmark Lending Rate, or EBLR, which is usually tied directly to the RBI Repo Rate).

If the RBI increases the repo rate to fight inflation, your home loan interest rate goes up. If the RBI cuts the repo rate, your home loan interest rate goes down.

The Pros:

- They start out 1% to 2% cheaper than fixed rates.

- Zero Prepayment Penalties: The RBI has banned banks from charging foreclosure fees on floating rate loans for individuals. This allows you to aggressively prepay your loan without friction.

- You automatically benefit when interest rates drop in the economy.

The Cons:

- Uncertainty. In 2022, when global inflation spiked, many Indian borrowers saw their floating rates jump from 6.5% to 9.0% in less than a year.

To see how a 2% change in interest rates affects your EMI and total payout, use our EMI Calculator:

3. The "EMI vs Tenure" Trap on Floating Loans

When interest rates rise on a floating loan, banks usually do not increase your monthly EMI amount because that could cause bounces. Instead, they silently increase your loan tenure.

If rates jump significantly, your 20-year loan might suddenly become a 28-year loan, and you won't even realize it unless you check your amortization schedule.

If this happens, you must manually instruct your bank to increase your EMI and keep the tenure exactly as it was.

4. The Verdict: Which Should You Choose?

In India, Floating Rate Home Loans are mathematically superior for 95% of retail borrowers.

Why? Because the average Indian closes their 20-year home loan in about 7 to 9 years through prepayments and balance transfers. The flexibility to prepay without massive 4% penalty charges is the single biggest advantage of a floating rate loan.

Furthermore, a 20-year window is long enough to ride out the interest rate cycles. The periods where rates are low usually offset the periods where rates are high, and since floating rates start cheaper, they generally win over the long run.

To calculate how fast you can close your floating rate loan with strategic prepayments, use our Home Loan Prepayment Calculator:

Related Reading

Put this into practice

Use our free interactive calculators to plan every aspect of your finances.

Table of Contents

You May Also Like

More articles about Loans & Debt Management

Home Loan EMI on ₹40 Lakh: The Complete Breakdown

Is a Credit Card Balance Transfer Good? The Hidden Costs Revealed

Personal Loan vs Car Loan: Which is Actually Cheaper?

Was this article helpful?

Master Your Money, Weekly.

Join 10,000+ Indians receiving our best wealth-building strategies, tax loopholes, and financial tool updates every Sunday. No spam, just value.

We respect your inbox. Unsubscribe anytime.