Advertisement

Do you remember your first salary? You probably earned ₹25,000 or ₹30,000 a month. Back then, you managed to pay rent, eat out occasionally, and survive perfectly fine.

Fast forward five years. You are now earning ₹80,000 a month. You make almost triple what you used to. By pure logic, you should be saving ₹50,000 a month, right?

Yet, somehow, your bank account is completely empty by the 25th of the month. You feel just as broke today on an ₹80,000 salary as you did on a ₹30,000 salary.

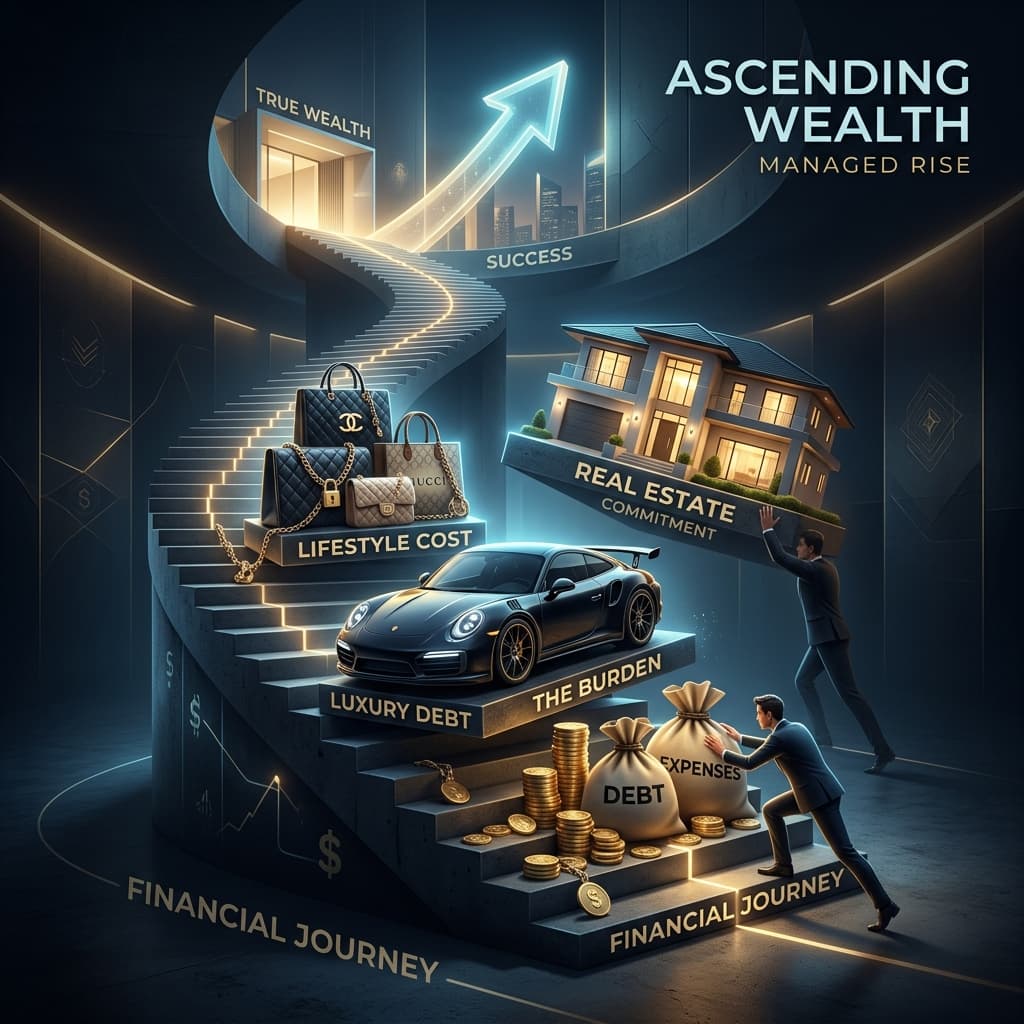

Welcome to Lifestyle Inflation (also known as Lifestyle Creep). It is the silent killer of wealth for the Indian middle class.

Key Takeaways

- The Definition: Lifestyle inflation occurs when your expenses rise exactly in proportion to your income. It is the financial equivalent of Parkinson's Law.

- The Upgrade Trap: It starts with a slightly nicer apartment, switches from Ola Mini to Ola Prime, and ends with a premium car EMI you cannot afford.

- The 50% Rule: To stop lifestyle creep, commit to saving exactly 50% of every future raise, bonus, or tax refund you receive.

- Track Net Worth: Focus on increasing your net worth, not just your visible lifestyle. Wealth is what you don't see.

Why Does Lifestyle Inflation Happen?

It isn't because you are suddenly irresponsible. Lifestyle inflation is deeply rooted in human psychology and social pressure.

1. Parkinson's Law of Money

Parkinson's Law states that "work expands to fill the time allotted for its completion." The financial version is: "Expenses rise to meet income." If you have ₹20,000 in your bank account, your brain automatically finds a way to spend exactly ₹20,000. If you have ₹1 Lakh, your brain will subconsciously rationalize buying premium brands and taking expensive vacations until that ₹1 Lakh is gone.

2. The "I Deserve It" Justification

When you get a promotion, you worked incredibly hard for it. You stayed late, you took on stress. Therefore, you tell yourself, "I deserve a nicer car" or "I deserve to eat at premium restaurants." While you do deserve to enjoy your money, using a one-time promotion to permanently lock yourself into higher monthly fixed costs (like a massive car EMI) is disastrous.

3. Peer Pressure and Status Signaling

As you move up the corporate ladder, the people around you change. Your new peers drive SUVs, wear branded watches, and send their kids to international schools. The pressure to conform and "signal" that you belong in this new wealth bracket is immense.

To see exactly how much this "upgrade" mentality is costing your future self, plug your numbers into our Lifestyle Inflation Calculator below:

The Devastating Impact on Retirement

Let's look at the math.

Arjun and Vikram both start working at 25, earning ₹50,000 a month. Both save 20% (₹10,000). Over the next 10 years, they both get promoted and now earn ₹1.5 Lakhs a month.

- Arjun (Victim of Lifestyle Inflation): Arjun upgrades his house, buys a Jeep Compass on EMI, and starts vacationing in Europe. He still saves exactly 20% of his new income (₹30,000).

- Vikram (Fights Lifestyle Inflation): Vikram stays in his modest flat, keeps driving his old hatchback, and only slightly upgrades his lifestyle. He saves 80% of his new raises. His new savings rate is ₹80,000 a month.

Because Arjun drastically increased his cost of living, his retirement corpus now needs to be massive to support his luxury lifestyle in old age. Vikram, on the other hand, kept his cost of living low. Not only did Vikram save dramatically more money, but his required retirement corpus is much smaller. Vikram can retire 15 years earlier than Arjun.

How to Stop Lifestyle Inflation (The 50% Rule)

You do not have to live like a monk when you get a raise. The goal of making money is to enjoy it. You just need a system to ensure your wealth grows alongside your lifestyle.

The easiest, most effective framework is the 50% Raise Rule.

Whenever you receive a raise, a bonus, or an unexpected windfall, you take exactly 50% of the new money and immediately direct it into your investments (SIPs). The remaining 50% can be used to upgrade your lifestyle guilt-free.

Example: If your take-home pay increases from ₹60,000 to ₹80,000, you have ₹20,000 of "new" money.

- ₹10,000 goes immediately into your mutual funds.

- ₹10,000 can be used to rent a better flat, upgrade your gym, or eat out more.

By doing this, your lifestyle improves visibly, but your wealth accelerates exponentially behind the scenes.

Shift Your Focus to Net Worth

The ultimate cure for lifestyle inflation is changing what you measure. Most people measure success by their job title and the car they drive.

Wealthy people measure success by their Net Worth (Assets minus Liabilities). When you obsess over your net worth, you get a dopamine hit every time your investment portfolio crosses a new milestone, rather than getting a dopamine hit from buying a designer jacket.

Track your actual wealth right now using our Net Worth Calculator:

Action Steps: How to Implement This Today

- Audit Your Last Raise: Think about your last salary hike. Did your savings amount actually increase, or did you just start spending more money on Swiggy and Uber?

- Automate the 50% Rule: If you are expecting an appraisal soon, log into your banking app before the new salary hits. Set up a new SIP for 50% of the expected hike amount.

- The 48-Hour Cart Rule: Stop impulse buying. If you want to buy a luxury item to "reward" yourself, leave it in your Amazon or Myntra cart for exactly 48 hours. If you still desperately want it after two days, buy it. 80% of the time, the urge will pass.

Related Reading

- How to Set Financial Goals Using the SMART Framework

- 10 Money Habits That Separate the Wealthy from the Broke

- The Latte Factor — Does Cutting Small Expenses Really Make You Rich?

[!CAUTION] Disclaimer: The content provided in this article is for educational and informational purposes only and does not constitute financial, investment, or tax advice. Always consult with a certified financial advisor or a registered tax consultant before making any financial decisions or filing your taxes.

Put this into practice

Use our free interactive calculators to plan every aspect of your finances.

Table of Contents

- Why Does Lifestyle Inflation Happen?

- 1. Parkinson's Law of Money

- 2. The "I Deserve It" Justification

- 3. Peer Pressure and Status Signaling

- The Devastating Impact on Retirement

- How to Stop Lifestyle Inflation (The 50% Rule)

- Shift Your Focus to Net Worth

- Action Steps: How to Implement This Today

- Related Reading